Ranked IV and vol context: shipped inside Option Chain Analysis

There is no separate Volatility Desk route. Cross-sectional IV rank, IV percentile, and vol-focused drawer tabs live on /app/option-chain-analysis with the same universe grid as GEX.

Volatility Desk was described earlier as a future /app/volatility-desk workspace. That route does not exist in the shipped product. Instead, cross-sectional volatility is columns and list sorts on the same page as dealer gamma: Option Chain Analysis at /app/option-chain-analysis.

Legacy URLs that used ?mode=vol, volRank, or volDrawerTab are rewritten client-side into the unified rank + drawerTab shape (for example vol drawer tabs such as vol-rank-overview). You stay on Option Chain Analysis—you do not switch to a second product URL.

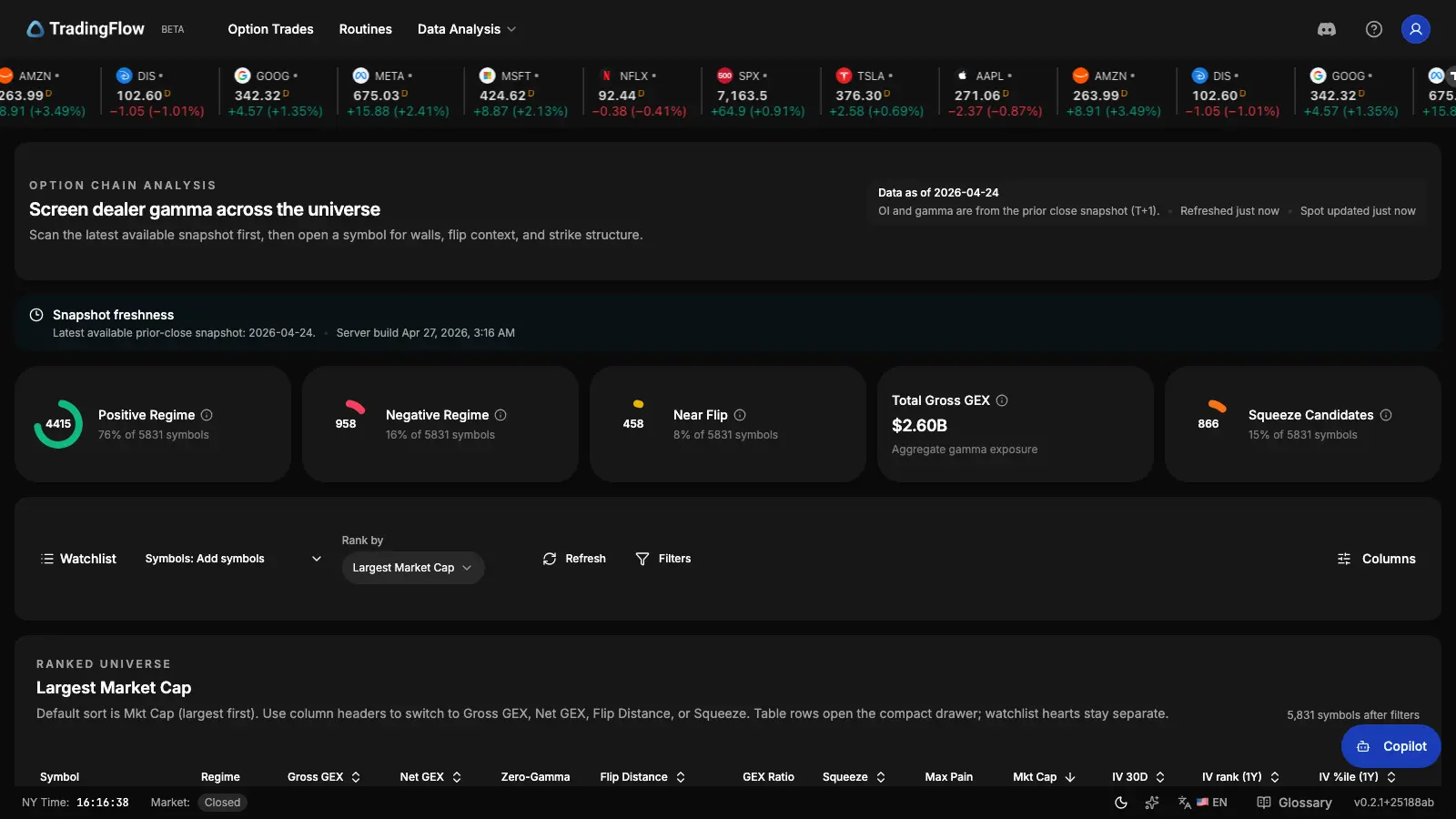

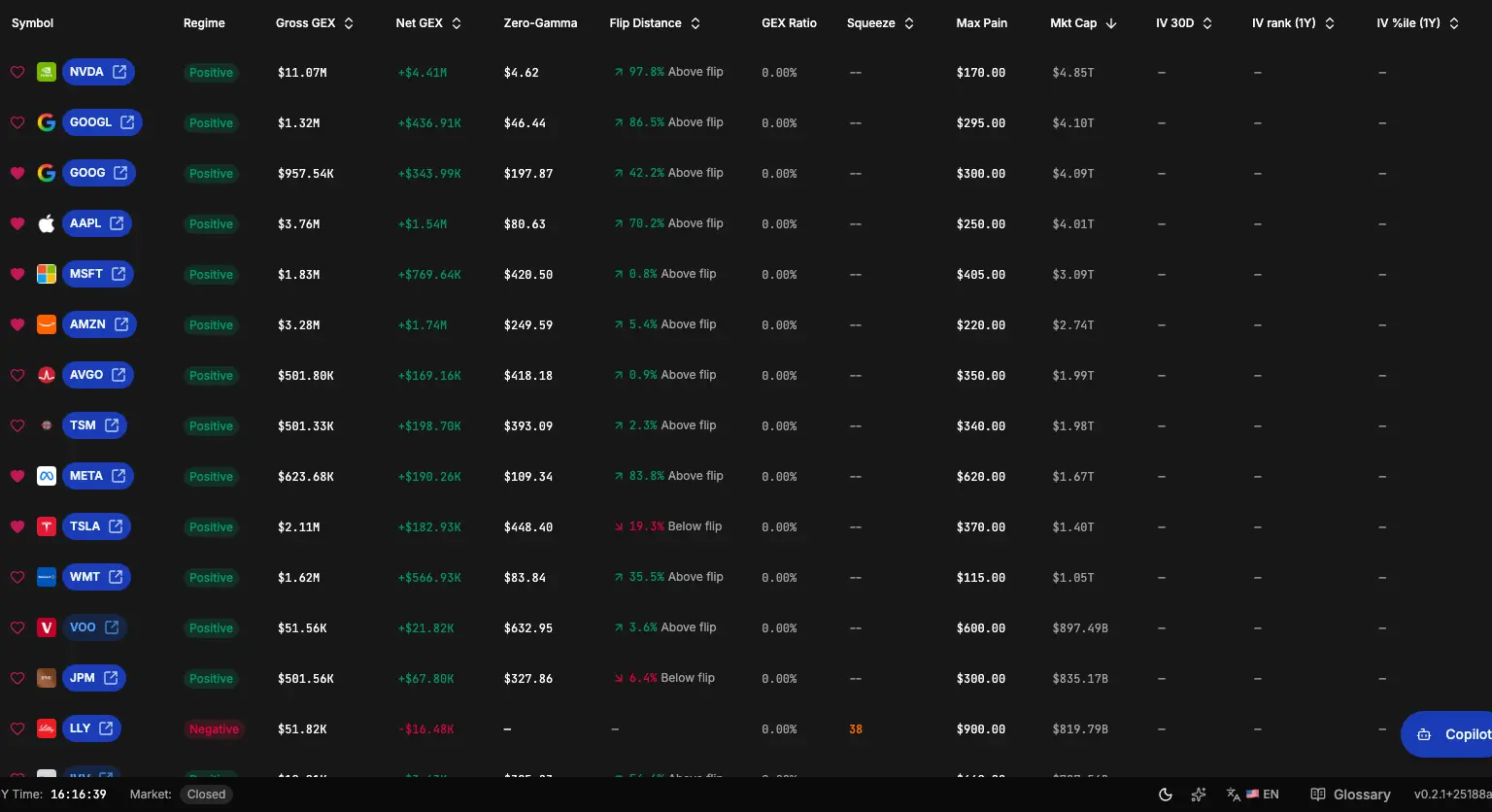

There is no separate /app/volatility-desk UI. The images below are captured from Option Chain Analysis—the same route where IV rank / percentile columns and vol list sorts ship today.

What ships today

- One universe table — GEX-style columns plus

iv30, 1y IV rank, and 1y IV percentile from the same snapshot-driven grid when those fields are populated. - Vol list sorts — Switch the list

rankto volatility modes such asiv_rankandiv_percentileon/app/option-chain-analysis(same table as gross/net/flip GEX sorts). - Vol-rank symbol drawer — When a vol sort is active, the drawer follows the vol-rank experience (for example Overview, Term structure, Earnings tabs). Deeper single-symbol vol analytics there may still be scaffolded; the grid is the primary cross-sectional vol surface today.

Legacy “planned” rank modes vs URL behavior

Older marketing tables listed modes like IV–HV spread, term slope, 25-delta skew, and earnings-style ranks as future desk modes. In the current URL contract, those legacy vol sort keys normalize to iv_rank if they appear in old links—they are not advertised here as first-class selectable modes unless the UI exposes them again. Rely on the in-app sort control for what is actually selectable.

Why one surface matters

Screener-first vol discovery runs next to GEX structure so you can answer “where is IV rich or cheap?” and “how are dealers positioned?” without changing routes. That matches the domain invariant: no separate Volatility Desk nav entry; discovery is sort and columns, not a parallel app.

Related workflows

- Option Chain Analysis —

/app/option-chain-analysis; GEX ranks, vol ranks, unifiedrank/drawerTablinks. - Gamma Exposure Screener (legacy name) — how the old GEX-only naming maps to the same route.

- Symbol-level analysis — flow-ranked symbols on

/app/market-rank. - Option Trades —

/app/option-tradesfor trade-level follow-up.

Follow the Roadmap and Changelog for future drawer and pipeline work; deep links should still target /app/option-chain-analysis, not /app/volatility-desk.

Related Articles

Option Chain Analysis: GEX, Volatility, and Per-Symbol Depth in One Surface

One route (`/app/option-chain-analysis`) combines GEX universe ranking, cross-sectional IV columns, and a symbol drawer—using a unified `rank` + `drawerTab` URL contract. GEX inspection includes OI Time Machine (`oi-timeline`); vol sorts open a vol-rank drawer (Overview, Term structure, Earnings).

OI Change Rank (retired): where cross-symbol OI ranking went

The standalone OI Change Rank app and /app/oi-change-rank are removed from the product (2026). Per-symbol OI history now lives in Option Chain Analysis as OI Time Machine in the symbol drawer.

Gamma Exposure Screener (legacy name) → Option Chain Analysis

The old Gamma Exposure Screener URL redirects to Option Chain Analysis. Same snapshot GEX universe, now with unified rank/drawer URLs and cross-sectional vol on one grid.